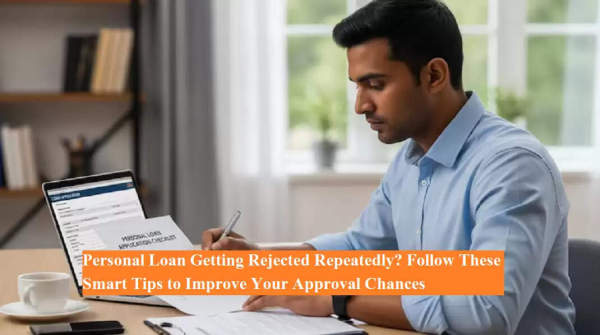

Personal loans often come as a financial savior during emergencies—whether it’s for medical expenses, education, travel, or debt consolidation. However, many applicants face repeated rejections due to small yet critical mistakes in their applications. Understanding what banks and financial institutions look for can significantly increase your chances of loan approval. Here’s a complete guide to help you ensure your personal loan is approved without unnecessary delays or rejections.

1. Maintain a Strong Credit Score

Your credit score is the most important factor determining whether your personal loan will be approved. It reflects your repayment history and overall financial reliability.

-

A score of 750 or above is generally considered ideal by most banks and NBFCs.

-

A high score indicates that you have repaid your previous loans or credit card bills on time, making you a low-risk borrower.

-

With a strong credit score, not only do you stand a better chance of quick approval, but you may also receive lower interest rates and higher loan amounts.

Tip: Check your credit score regularly through official credit bureaus. If you notice any discrepancies or outdated data, get them corrected immediately. Paying EMIs and credit card dues on time can gradually boost your score.

2. Ensure Job Stability and Steady Income

Banks prefer lending to applicants with a stable job and regular income. Before approving your loan, lenders verify your employment type, salary consistency, and the reputation of your employer.

If you’ve been working continuously for at least 1–2 years in a reputable company, your profile is considered more reliable. Salaried professionals in government or established private firms are often given preference over self-employed individuals, as their income sources are viewed as more stable.

Tip: Avoid switching jobs too frequently and maintain a consistent income flow. If you’re self-employed, ensure your financial records and ITR filings are up-to-date to prove steady earnings.

3. Keep Your Debt-to-Income Ratio Low

Banks assess how much of your income is already committed to existing loans and EMIs. Ideally, your total EMIs should not exceed 40–50% of your monthly income.

If a major portion of your income is already going towards loan repayments, lenders might reject your new loan application, assuming a higher repayment risk.

Tip: Try clearing smaller loans or credit card dues before applying for a new personal loan. Reducing your EMI burden improves your repayment capacity and enhances your approval chances.

4. Age Matters—Apply Within the Eligible Range

Most lenders offer personal loans to individuals aged between 21 and 60 years. This age bracket is considered financially active, with a stable earning potential.

If you’re nearing retirement or just starting your career, lenders may see higher risk, which can lead to rejections or smaller loan amounts.

Tip: If you are younger, build a credit history by using a credit card responsibly. If you are older, showcase your steady income or pension proofs to strengthen your application.

5. Additional Smart Tips for Smooth Approval

-

Pay all EMIs and credit card bills on time. Delays or defaults can instantly lower your creditworthiness.

-

Avoid multiple loan applications simultaneously. Every rejection or inquiry affects your credit score negatively.

-

Keep your documents ready. Banks require KYC details, salary slips, bank statements, and proof of employment. Ensure all documents are up-to-date and accurate.

-

Plan your borrowing wisely. Apply only for the amount you genuinely need and can comfortably repay.

Final Thoughts

Getting your personal loan approved isn’t just about applying at the right time—it’s about presenting yourself as a reliable borrower. Maintaining a good credit score, stable income, low debt ratio, and strong financial discipline will not only help your application get approved faster but also allow you to negotiate better terms.

By following these essential steps and staying financially disciplined, you can make your next loan approval almost guaranteed—ensuring that when the need arises, money is never out of reach.

-

British Sikh group prepares for judicial review of Islamophobia definition

-

Majority of leading Higher Education Institutions in India allow AI use: Report

-

UP teenager blinded in one eye after police brutality over mosque announcement

-

Raghav Juyal reveals SRK and Aryan’s reaction to Samay’s bold T-shirt

-

Gill or Rohit … with whom does Sapna Chaudhary want to share the stage? Revealed yourself