Filing your Income Tax Return (ITR) for the first time can feel confusing—especially when terms like exemption, deduction, and rebate come into play. Many taxpayers miss out on legitimate tax savings simply because they don’t clearly understand these concepts.

If you want to reduce your tax legally and file your ITR with confidence, understanding these three terms is essential. Here’s a simple and clear breakdown to help you avoid confusion and maximize savings.

Why These Terms Matter in ITR FilingThe Income Tax Department of India provides several provisions to help taxpayers reduce their tax burden. Exemption, deduction, and rebate are three key tools—but they work at different stages of tax calculation.

Understanding where each one applies can make a big difference in your final tax liability.

What Is Exemption? (Income Not Taxable)Exemption means a portion of your income is completely tax-free.

👉 This income is excluded before calculating taxable income.

Examples of Exemption:- Agricultural income

- House Rent Allowance (HRA) (under conditions)

- Certain allowances and benefits

📌 Impact: Your total income itself gets reduced before tax calculation.

What Is Deduction? (Reduce Taxable Income)Deduction allows you to subtract certain investments or expenses from your total income.

👉 This happens after calculating total income but before applying tax rates.

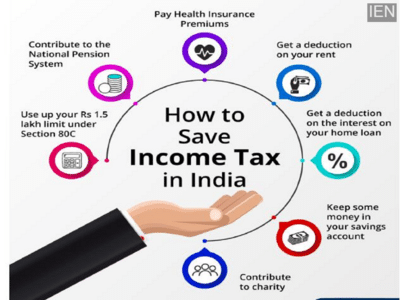

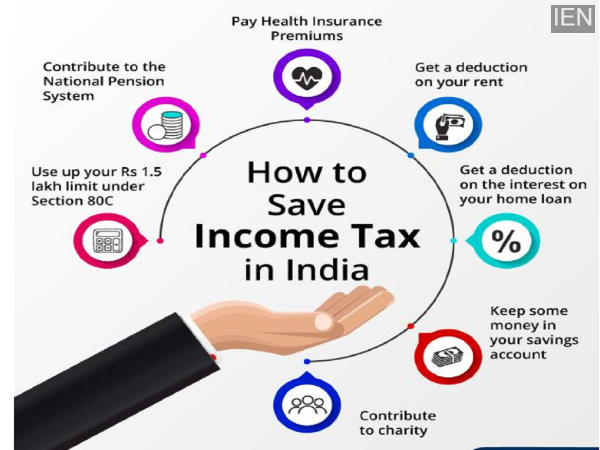

Popular Deductions:- Section 80C (LIC, PPF, ELSS) – up to ₹1.5 lakh

- Section 80D (Health insurance premium)

- Section 24 (Home loan interest)

📌 Impact: Your taxable income becomes lower, so you pay less tax.

What Is Rebate? (Reduce Final Tax Amount)Rebate is applied after your tax has already been calculated.

👉 It directly reduces your final tax payable.

Example:- Under Section 87A:

- New tax regime → Up to ₹60,000 rebate (income up to ₹12 lakh)

- Old tax regime → ₹12,500 rebate (income up to ₹5 lakh)

📌 Impact: Your final tax bill is reduced—even to zero in some cases.

Key Difference Between Exemption, Deduction & Rebate| Exemption | Before tax calculation | Removes income from tax |

| Deduction | Before tax calculation | Reduces taxable income |

| Rebate | After tax calculation | Reduces final tax amount |

If used smartly, all three can significantly lower your tax:

- Use exemptions to exclude eligible income

- Claim deductions through investments and expenses

- Apply rebate to reduce final tax liability

💡 Combining all three properly can even bring your tax down to zero in some cases.

Final TakeawayUnderstanding exemption, deduction, and rebate is the key to smart tax planning. While they may sound similar, each plays a different role in reducing your tax burden.

Before filing your ITR, take a few minutes to review these concepts. A clear understanding can help you save more tax legally and make the entire filing process much smoother.

👉 Smart planning today means more savings in your pocket tomorrow.

-

White House Dinner Shooting Suspect Was Armed With 'Multiple Weapons', Says Trump

-

MI Vs CSK At Wankhede Stadium In Mumbai: Here Are The Iconic South Indian Eateries Nearby To Visit

-

Sachin Tendulkar, VP Radhakrishnan And CM Chandrababu Naidu To Grace Andhra University's Centenary Celebrations On April 27

-

Sushant Singh Rajput Death Case: Special NDPS Court Orders Defreezing Of Rhea Chakraborty, Brother’s Bank Accounts; Flags NCB Lapses

-

Sanjay Dutt, Anil Kapoor And Sunny Deol: No longer 'The Expendables