While planning for retirement, we meticulously account for every single rupee; however, are you aware that the money you deposit sometimes never actually reaches your Permanent Retirement Account Number (PRAN)? Several instances have come to light within the National Pension System (NPS) where subscribers deposited funds through a 'Point of Presence' (PoP), only for that money to get stuck due to technical glitches or the cancellation of an intermediary's registration.

The good news is that the PFRDA has established a 'Subscribers’ Pension Contribution Protection Account' (SPCPA) to safeguard such 'unclaimed' funds. The objective of this account is to protect the interests of subscribers and ensure the return of their money, along with accrued interest. If your funds have also been stuck for years, you can claim them at any time within a 25-year window. Let us understand the entire process. The PFRDA has made the procedure for retrieving stuck NPS funds highly transparent and systematic.

Great News for Central Government Employees! If Pension is Delayed, the Government Will Pay a 'Heavy Penalty'—Accruing Interest Equivalent to PPF Rates (7.1%)

Add Zee Business as a Preferred Source

What is the SPCPA Account?

The SPCPA is a specialized protection account administered by the PFRDA. When a contribution remains unclaimed for a period of 7 years or more, it is transferred into this account. It serves as a form of 'safe custody' for funds that could not be successfully matched with a subscriber's PRAN.

Who Can Apply for a Refund?

Subscribers whose funds were deposited with a PoP but were not credited to their PRAN.

Cases where a contribution was made, but a PRAN could not be generated.

Instances where an intermediary's license was revoked, leaving the funds in limbo.

The 'Homecoming' of the Old Pension Scheme! Officers Recruited After 2004 to Also Receive Benefits of OPS; Centre Issues New Rules

Step-by-Step Process for Filing a Claim

Step 1: Filing the Application

The subscriber must submit a formal application for a refund. This application can be sent directly to the PFRDA or submitted through the concerned PoP-NPS. Remember, you may file a claim within 25 years from the date the funds were transferred.

Step 2: Attaching Supporting Documents

Along with the application, you must attach necessary documents such as proof of investment (e.g., receipts), identity proof, and bank account details.

Step 3: Verification Process

The PFRDA will closely scrutinize the documents submitted by you. If any discrepancy is detected, the matter may be referred back to the intermediary for verification.

Step 4: Approval and Refund

Once the verification process is completed, the PFRDA will approve the refund.

Interest Payout

Most importantly, you will not receive merely the principal amount. Interest for the entire duration—during which the funds remained deposited in the SPCPA account—will also be paid at a rate determined by the Authority. Furthermore, if an error on the part of the intermediary is established, the subscriber may also be entitled to receive compensation recovered from that intermediary.

Disclaimer: This content has been sourced and edited from Navbharat Times. While we have made modifications for clarity and presentation, the original content belongs to its respective authors and website. We do not claim ownership of the content.

-

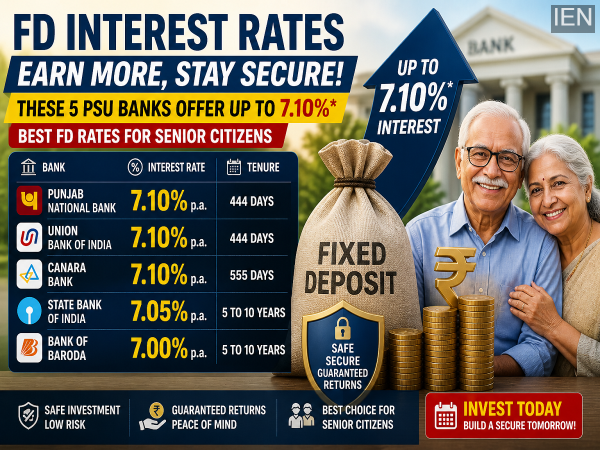

Best FD Rates in May 2026: These 5 PSU Banks Offer Up to 7.10% Interest for Senior Citizens

-

SBI Bank Strike Alert: Services May Be Hit for 4 Days in May—Check Dates Before Visiting Branch

-

₹15,000 Monthly Expense Today—How Much Will You Need After 20 Years? Full Inflation Calculation Explained

-

8th Pay Commission Update: ₹65,000 Minimum Salary Demand Raised in Pune Meet, Big HRA & Allowance Changes Proposed

-

What Is Circle Rate? How It Determines Property Value, Taxes, and Home Loan—Full Guide for Buyers