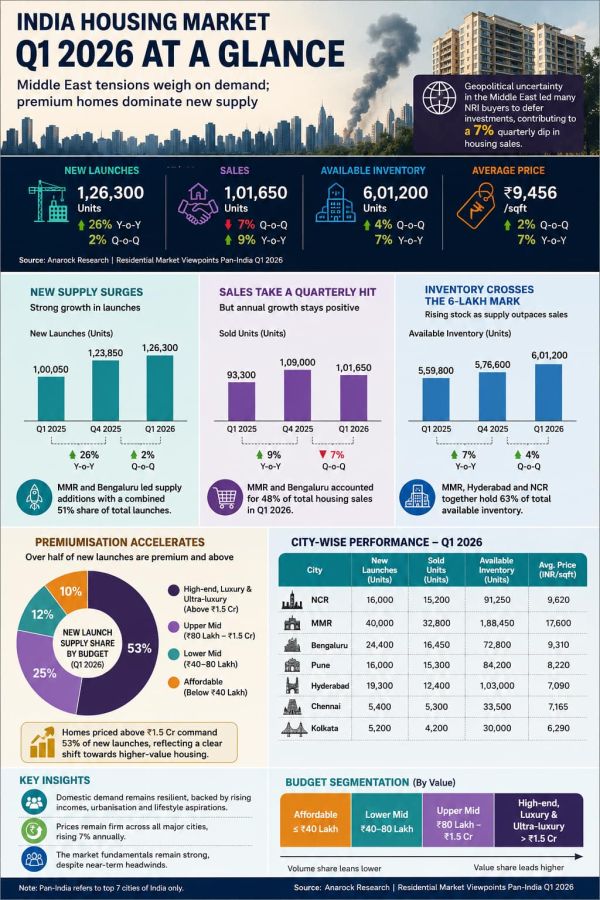

India’s residential property market entered 2026 with a mixed picture. While premium homes continue to dominate new launches and prices remain firm across major cities, the ongoing conflict in West Asia has begun to weigh on buyer sentiment, particularly among Non-Resident Indian (NRI) investors from West Asia.

According to Anarock’s ‘Residential Market Viewpoints Q1 2026’ report, housing sales across India’s top seven cities fell 7 per cent quarter-on-quarter in Q1 2026 to around 1,01,650 units, down from nearly 1,09,000 units in the previous quarter. fileciteturn8file0

The report attributes the slowdown largely to geopolitical uncertainty linked to the West Asian conflict, which has pushed up oil prices, increased construction costs and triggered caution among homebuyers.

West Asia Conflict Begins To Impact Housing Sentiment

The report noted that the March quarter saw buyers adopt a more cautious approach amid rising geopolitical tensions.

“Prospective Middle Eastern NRI homebuyers, who invest significantly in Indian real estate, appear to have temporarily deferred investment decisions amid geopolitical uncertainty,” the report said.

The impact appears particularly significant because West Asian NRIs remain an important buyer category in India’s premium and aspirational housing segments.

Higher crude oil prices have also had a cascading effect on the sector by increasing construction and input costs, prompting developers to focus on higher-margin projects.

Premium Housing Takes Centre Stage

Despite the softer sales momentum, developers have continued to aggressively launch premium projects.

Homes priced above Rs 1.5 crore accounted for 53 per cent of all new launches during Q1 2026, according to the report.

This included high-end homes priced between Rs 1.5 crore and Rs 2.5 crore, luxury housing in the Rs 2.5 crore to Rs 4 crore bracket, and ultra-luxury homes priced above Rs 4 crore.

The shift highlights how developers are increasingly prioritising profitability over volume amid rising land and construction costs.

“The composition of new supply in Q1 2026 reflects a clear shift towards higher-value housing segments,” the report stated.

At the same time, affordable housing continued to lose ground. Homes priced below Rs 40 lakh accounted for just 10 per cent of new launches, while the lower-mid segment contributed 12 per cent.

Developers Keep Launching Despite Sales Dip

Even as sales slowed, developers maintained strong launch momentum.

New residential launches across the top seven cities rose 26 per cent year-on-year and 2 per cent sequentially to approximately 1,26,300 units in Q1 2026. fileciteturn8file0

Mumbai Metropolitan Region (MMR) led launch activity with around 40,000 units, followed by Bengaluru with 24,400 units and Hyderabad with approximately 19,300 units. Together, MMR and Bengaluru accounted for more than half of the total new supply additions.

However, the widening gap between launches and actual sales has started showing up in inventory levels.

Unsold Inventory Crosses 6 Lakh Units

Available housing inventory across the top seven cities crossed the six-lakh mark for the first time in recent quarters, reaching approximately 6,01,200 units by the end of Q1 2026.

According to the report, this increase reflects “healthy developer launch momentum meeting a moderated absorption pace”.

Inventory overhang also increased to around 18 months nationally, compared with 17 months in the previous quarter. Hyderabad recorded the highest inventory overhang at 26 months, while Bengaluru maintained the lowest at 14 months due to stronger end-user demand.

Prices Stay Firm Despite Global Uncertainty

Interestingly, home prices continued to rise despite softer sales.

Average residential prices across the top seven cities rose 7 per cent year-on-year and 2 per cent quarter-on-quarter, increasing from Rs 8,868 per square foot in Q1 2025 to Rs 9,456 per square foot in Q1 2026.

NCR recorded the steepest annual price rise at 15 per cent, driven largely by luxury and ultra-luxury launches. Bengaluru saw an 8 per cent annual increase, while other major cities registered moderate gains.

Senior Living and Co-Living Emerge as New Themes

Beyond luxury housing, the report also flagged changing buyer preferences and evolving housing formats.

Senior living and age-targeted housing are expected to emerge as a distinct category, with developers increasingly carving out dedicated projects within larger townships.

At the same time, co-living and flexible housing formats are expected to expand in major employment hubs, driven by migration into technology and services corridors.

Long-Term Demand Story Remains Intact

Despite the near-term geopolitical disruption, the report maintained that India’s long-term housing demand story remains strong.

Anarock Chairman Anuj Puri said domestic demand continues to hold up, supported by rising incomes, urbanisation and aspirations for lifestyle upgrades.

The report added that the current slowdown appears more like a temporary pause rather than a structural weakening of the housing market.

Looking ahead, developers are expected to focus more on project execution and timely delivery instead of aggressive launches, especially as elevated construction costs continue to pressure margins.

-

Arshdeep's Girlfriend Samreen Was Earlier Linked With This Youtube Superstar

-

Apple's Next AirPods May Have Cameras, But There's A Catch

-

‘Bengal’s Dream Has Come True’: Amit Shah Celebrates BJP’s Historic Election Victory

-

Suvendu Adhikari’s Swearing-In As Bengal CM Tomorrow; PM Modi, NDA CMs To Attend

-

Aakhri Sawal Trailer Out: Sanjay Dutt Faces Tough Questions On Gandhi, Babri And Emergency