Ambuja’s quarterly performance was driven by continued demand and improvement in cement sales volumes. Revenue increased to Rs 10,915 crore in Q4 from Rs 10,277 crore in Q3, while volumes increased to 19.9 million tonnes from 18.9 million tonnes. On a year-on-year basis, volumes increased 10% to 18.2 million tonnes, indicating continued market momentum. However, EBITDA declined 22% year-on-year to Rs 1,464 crore, reflecting pressure on margins due to higher fuel and operating costs.

Growth continued to be strong, with EBITDA increasing from Rs 1,353 crore in Q3 to Rs 1,464 crore in Q4, an increase of 8%. EBITDA per tonne also increased to Rs 735 from Rs 718 in the previous quarter. The company faced cost constraints in the quarter due to increased expenses on electricity, fuel, logistics and packaging, which impacted profits as compared to last year.

The reported profit growth was significantly impacted by certain items such as tax adjustments and one-time benefits. Normalized profit stood at Rs 569 crore in Q4 FY26, compared to Rs 414 crore in Q3 and Rs 856 crore in Q4 FY25. Earnings per share rose to Rs 7.37 from Rs 0.97 in the previous quarter and Rs 4.16 a year ago, showing consistent improvement.

For full year FY26, Ambuja reported revenue of Rs 40,656 crore, up 15 per cent year-on-year, while net profit rose to Rs 5,637 crore. Cement volumes grew 16 per cent this year to 73.7 million tonnes, reflecting strong operational momentum and increased capacity utilisation. The company’s performance reflects stable demand conditions, although margin pressure from input costs continues to weigh on earnings quality. Operational efficiency and volume growth remain the key contributors to performance.

-

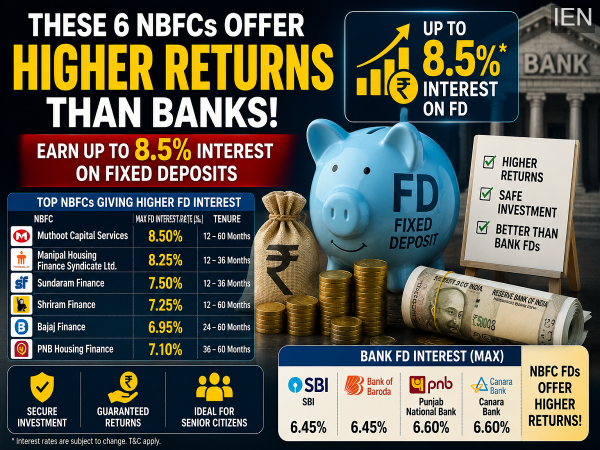

These 6 NBFC FDs Are Offering Higher Returns Than Banks, Earn Up to 8.5% Interest

-

8th Pay Commission Talks Intensify: Major Decisions on Salary, Pension and Allowances Expected Soon

-

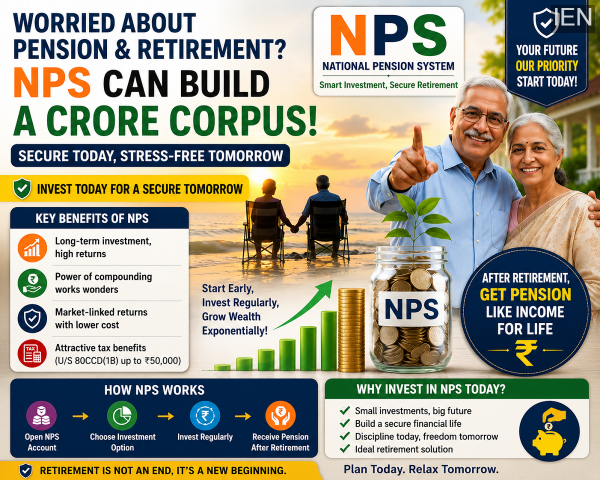

Build a Massive Retirement Corpus with NPS, Secure Your Pension and Financial Future

-

Want to Save More Tax? These 4 Investment Options Can Help You Save Lakhs Legally

-

Sohail Khan Announces My Punjabi Nikaah With Sanjay Dutt And Aayush Sharma