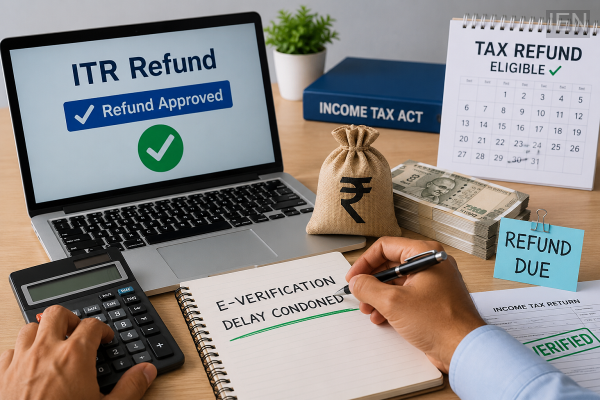

Taxpayers who filed their Income Tax Return (ITR) on time but completed the mandatory e-verification after the prescribed deadline may still be eligible for a refund, provided the delay has been officially condoned. In a significant ruling, the Delhi Income Tax Appellate Tribunal (ITAT) has clarified that tax authorities cannot reject or withhold a legitimate refund solely because the return was e-verified late after the delay has already been accepted by the Income Tax Department.

The decision offers important relief to taxpayers who miss the e-verification deadline due to genuine circumstances but later obtain approval for condonation of delay.

ITAT Provides Relief to Taxpayers

In its recent order, the Delhi ITAT observed that once the Central Processing Centre (CPC) condones the delay in completing e-verification, the Income Tax Department cannot continue to rely on the same procedural lapse to deny a refund.

The tribunal further stated that if a taxpayer has no outstanding tax liability, retaining the refund amount without legal justification would be inconsistent with the principles laid down under Article 265 of the Constitution of India, which states that no tax can be imposed or collected except by the authority of law.

According to the tribunal, withholding money that rightfully belongs to a taxpayer without any legal basis is not permissible.

Background of the Case

The case involved a Delhi-based taxpayer who filed an Income Tax Return for Assessment Year 2015-16 within the due date under Section 139(1) of the Income Tax Act.

While filing the return, the taxpayer claimed the adjustment of current-year losses, unabsorbed depreciation, and brought-forward losses from previous years. After these adjustments, the taxable income became nil.

The taxpayer also claimed an income tax refund of approximately ₹17.08 lakh, largely representing Tax Deducted at Source (TDS) on rental income.

However, the return was not electronically verified within the prescribed timeline, resulting in procedural complications.

Why the E-Verification Was Delayed

During the proceedings, the taxpayer informed the tribunal that the delay occurred because his 83-year-old father was critically ill and required frequent hospitalization. Owing to these exceptional personal circumstances, the taxpayer could not complete the e-verification process within the stipulated period.

Later, the taxpayer submitted an application requesting condonation of the delay before the Central Processing Centre.

The CPC accepted the request and officially condoned the delay. Following this approval, the return was successfully e-verified on 16 February 2018.

Despite this, the Income Tax Department did not process the return under Section 143(1), and the refund remained unpaid.

Appeals Before Reaching ITAT

After the refund was not issued, the taxpayer filed a rectification application under Section 154 of the Income Tax Act.

The Assessing Officer rejected the request. Subsequently, the first appellate authority also upheld the department's decision.

The taxpayer then approached the Delhi Income Tax Appellate Tribunal seeking relief.

Tribunal's Observations

After examining the facts, the ITAT ruled in favour of the taxpayer.

The tribunal noted that there was no dispute regarding the deduction of TDS, and the relevant records were already available with the Income Tax Department.

It also observed that the CPC had already condoned the delay in e-verification. Therefore, continuing to deny the refund on the same technical ground was unjustified.

According to the tribunal, where no tax liability exists, withholding the taxpayer's money would amount to unjust enrichment by the government.

The order also referred to Article 265 of the Constitution, emphasizing that tax authorities cannot retain money without legal authority simply because of a procedural technicality.

Refund Cannot Be Denied on Technical Grounds Alone

The ITAT set aside the orders passed by the lower authorities and directed the Assessing Officer as well as the Central Processing Centre to take the necessary legal steps for issuing the refund in accordance with applicable laws.

The tribunal made it clear that once the delay in e-verification has been formally condoned, the department cannot continue to use that delay as the sole reason for refusing to process a valid refund claim.

What This Means for Taxpayers

The ruling highlights the importance of the condonation process for taxpayers who miss the e-verification deadline due to genuine reasons.

However, the decision does not mean that every delayed e-verification will automatically qualify for a refund. The tribunal specifically noted that the taxpayer in this case had:

-

Filed the Income Tax Return within the prescribed due date.

-

Successfully obtained condonation of the delayed e-verification from the CPC.

-

Had no outstanding tax liability.

-

Had valid TDS records already available with the Income Tax Department.

Therefore, the judgment is based on the specific facts of this case. Taxpayers facing similar situations should ensure that the delay is formally condoned by the department before seeking relief.

The ruling nevertheless reinforces the principle that procedural lapses alone should not deprive taxpayers of refunds legally due to them once the prescribed legal requirements have been satisfied.

-

Why are homosexuals demanding the right to marry? Property-inheritance rights, medical decisions, adoption rights and more

-

Microsoft launches Frontier Company with $2.5 billion to help businesses adopt AI

-

Now your Digital Signature will be saved in the phone itself! Google coming soon with a new app? How will users benefit? find out

-

Jurgen Klopp Set To Become Germany Football Team Head Coach After FIFA World Cup 2026 Debacle

-

FIFA World Cup 2026: Double Thrill at World Cup; Norway’s challenge in front of Brazil, England’s fight with Mexico, who will win?