Wall Street sees bigger upside in VKTX, with Koyfin’s average target implying 120% upside versus 99% for BCRX.

- Vertex’s $10B Crinetics buy has revived mid-cap biotech M&A speculation, putting VKTX and BCRX back in focus.

- BCRX has the cleaner M&A focus, given its rare-disease focus, Orladeyo franchise, Navenibart pipeline and prior Betaville chatter.

- But VKTX may offer the bigger catalyst-driven setup, with Q3 VK2735 maintenance data, oral VK2735, VK3019 and the mid-to-late 2027 Vanquish readout ahead.

Vertex Pharmaceuticals’ (VRTX) acquisition of Crinetics Pharmaceuticals (CRNX) has turned the spotlight back on mid-cap biotech, where Viking Therapeutics’ (VKTX) obesity pipeline and BioCryst Pharmaceuticals’ (BCRX) rare-disease platform are drawing fresh takeover buzz.

VKTX stock jumped 9% on Tuesday, while BCRX shares climbed 8% as traders piled into biotech stocks seen as potential winners from a revived M&A cycle. The spark was Vertex’s agreement to buy Crinetics for $85 per share in cash, valuing the deal at about $10 billion. The offer represented a 102% premium to Crinetics’ previous close and gave Vertex a bigger foothold in rare hormonal diseases. For investors, the signal was that Big Pharma is still willing to pay up for the right biotech asset.

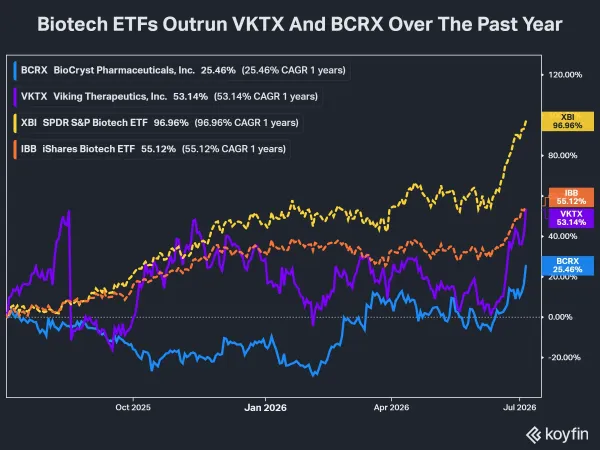

Over the past year, both VKTX and BCRX have gained ground, though their returns trail the broader biotech ETF rally. VKTX shares are up 53%, while BCRX has risen 25%. By comparison, the iShares Biotechnology ETF (IBB) is up 55%, and the SPDR S&P Biotech ETF (XBI) has surged 97%.

Wall Street Sees Bigger Upside In VKTX

On Wall Street’s upside math, Viking comes out ahead. Koyfin data shows VKTX’s average 12-month target of $92.58 implies a 120% upside from current levels. The stock has 20 covering analysts: five 'Strong Buy' ratings, 13 'Buy' ratings, two 'Hold' ratings, and no 'Sell' or 'Strong Sell' ratings. Koyfin lists its overall rating as 'Strong Buy.'

BCRX also leans bullish, but with slightly lower upside. Its average 12-month target of $21.90 implies a 99% upside from current levels. The stock has 10 covering analysts: three 'Strong Buy' ratings, seven 'Buy' ratings, and no 'Hold,' 'Sell' or 'Strong Sell' ratings. Koyfin also lists BioCryst’s overall rating as 'Strong Buy.'

The latest Wall Street commentary gives both stocks another reason to stay in the spotlight. For Viking, Piper Sandler reiterated an 'Overweight' rating and $71 price target, implying a 69% upside from the stock’s last close. The firm called Viking’s third-quarter (Q3) subcutaneous maintenance data for its lead drug VK2735 an ‘underappreciated’ catalyst.

For BioCryst, Wedbush said investors should watch commercial-stage rare and endocrine-disease stocks such as BioCryst and Ascendis Pharma as potential next targets after Vertex’s Crinetics deal, citing the rich premium paid. RBC Capital also raised its price target on BioCryst to $14 from $13 and kept an 'Outperform' rating on the shares. That $14 target implies 27.4% upside from BioCryst’s current price of $10.99.

BCRX Gets Boost From Rare-Disease Deal Chatter

BioCryst looks like the more obvious stock to benefit from the Vertex-Crinetics deal. The company already has a commercial rare-disease business led by Orladeyo, an oral medicine that helps prevent attacks of hereditary angioedema, or HAE, a rare disorder that causes sudden swelling episodes. The company is also developing Navenibart, a long-acting injectable antibody designed to prevent HAE attacks.

Recent European Academy of Allergy and Clinical Immunology (EAACI) data kept both assets in focus. Orladeyo showed sustained reductions in pediatric HAE attacks over 48 weeks, with no significant safety concerns, while Navenibart reduced attacks across key patient subgroups. BioCryst has also sharpened its strategy, moving to discontinue internal discovery programs and close its Birmingham, Alabama discovery facility by the end of 2026.

BioCryst had already drawn M&A speculation in March after a Betaville “uncooked” alert suggested a U.S.-based biopharma company with a market value above $15 billion may have shown interest in the company.

VK2735 Gives Viking A Major Q3 Catalyst

On the other hand, Viking is not at the commercial stage, and it is not a rare-disease company. But it may have a more attractive fundamental setup. Viking is one of the more closely watched obesity-drug developers in biotech. Its lead candidate, VK2735, is a dual GLP-1/GIP receptor agonist being developed in both injectable and oral forms.

Viking’s market cap stands at about $4.89 billion, making it larger than BioCryst but still squarely in mid-cap biotech territory. As of March 31, the company had $603 million in cash, cash equivalents and short-term investments, down from $706 million last year. Viking has said that cash position gives it runway through 2028, enough to fund ongoing Phase 3 obesity trials and key milestones.

Viking’s next key catalyst is Q3 2026 maintenance data for VK2735, which will test whether the obesity drug can support monthly or quarterly dosing after initial weight loss. Piper Sandler said VK2735’s 21-week induction phase will give investors the longest look yet at the drug, with weight loss above 15% to 16% versus placebo at Week 21 seen as highly competitive. Stable or further weight loss through Week 33 would support less frequent maintenance dosing.

The bigger event is the Phase 3 Vanquish readout, expected in mid-to-late 2027. Viking also has oral VK2735, which showed up to 12.2% weight loss at 13 weeks, and VK3019, a Phase 1 obesity candidate.

How Do Retail Traders Feel About VKTX And BCRX?

On Stocktwits, retail interest in both tickers has picked up sharply. VKTX sentiment flipped to ‘bullish’ from 'bearish' a day earlier as 24-hour message volume jumped 400%, while monthly message volume surged 2,786%. Watchers for the ticker are also up 16% over the past year.

BCRX saw a similar spike in attention, with sentiment turning ‘extremely bullish’ from 'neutral' a day ago as 24-hour message volume rose 312%. Message volume has surged 2,763% over the past year, while ticker watchers are up 2% over the same period.

Several users said BCRX’s Orladeyo growth, Navenibart pipeline and rare-disease M&A demand could support a $30-$40-plus takeout case, while others pointed to Crinetics’ rich premium and unconfirmed Betaville chatter as reasons BCRX could draw renewed buyout interest. Users also speculated that a potential Amazon partnership could be a major upside catalyst for VKTX, with some relating the chatter to Amazon’s recent $25 billion bond sale.

For updates and corrections, email newsroom[at]stocktwits[dot]com.<

-

Gary Neville delivers blunt verdict on Lisandro Martinez’s performance against Egypt

-

ITV pundits, commentators, and presenters confirmed for Switzerland vs Colombia clash

-

Here is the salary received by Ram Mandir priests and staff; medical leave facilities are also provided..

-

From loco pilots to TTEs—what are the salaries of various railway employees?

-

IIT and NIT Salary Packages: These are the highest salary packages at IITs and NITs; the record stands at ₹3.67 crore..