It was FY22 and Shadowfax was still viewed largely as another fast-growing logistics startup battling for ecommerce deliveries in India’s crowded third-party logistics (3PL) market. Four years later, the Bengaluru-based company’s market share in the 3PL segment has climbed from roughly 8% to as much as 29%, making it one of the country’s largest logistics platforms.

But its ambitions now extend far beyond parcel delivery. After posting its first meaningful quarterly profit in Q4 FY26, Shadowfax is attempting something more consequential — transforming itself from a courier network into what its executives describe as a full-stack logistics operating system for India’s digital economy.

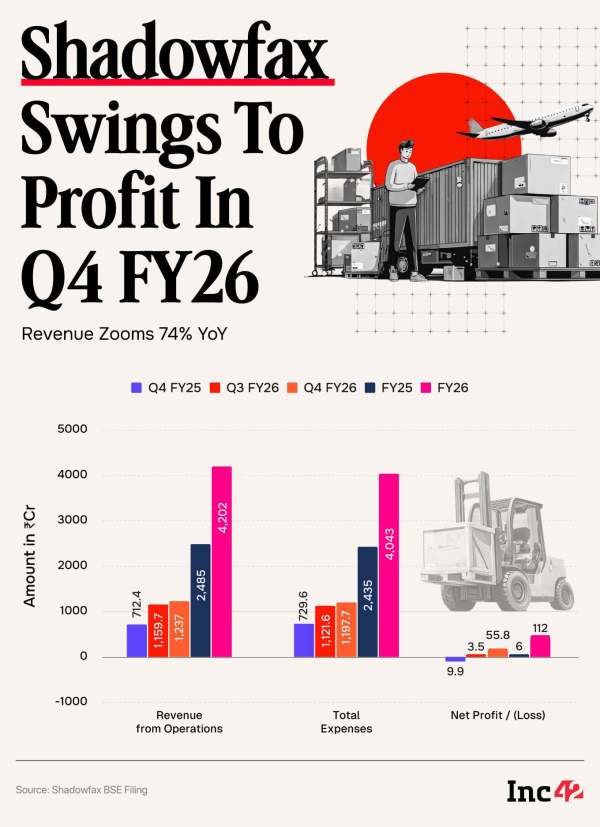

In the March 2026 quarter, Shadowfax reported revenue of ₹1,237 Cr, up 73.6% year-on-year (YoY), while net profit swung to ₹55.8 Cr from a loss of ₹9.9 Cr a year earlier. Adjusted EBITDA rose more than tenfold to ₹58 Cr, with EBITDA margin expanding to 4.7% from just 0.7% last year.

Operationally, the company delivered 22.6 Cr orders during the quarter, a staggering 100.8% jump from the prior year.

For most logistics companies, this combination — hypergrowth alongside expanding profitability — is difficult to achieve simultaneously. Yet Shadowfax executives insist the company is still early in its scale-up phase.

“We have hit a critical volume,” the startup’s management said during a post-earnings call, arguing that future automation investments will now break even “significantly faster”.

India’s logistics market has historically been fragmented, populated by regional delivery firms, captive logistics operations, and VC-funded startups competing aggressively on pricing. But this structure appears to be changing rapidly.

“What is happening in the industry is that the top two players continue to gain market share, and the market is becoming more and more consolidated,” Shadowfax’s management said on the earnings call.

The company believes its market share gains are coming from two directions simultaneously. Smaller third-party logistics providers are struggling to compete with scaled infrastructure networks, while large enterprises are increasingly reassessing if operating logistics in-house still makes economic sense.

The company’s management estimates that roughly 55% of its future growth will come from expansion of India’s underlying digital commerce economy, while another 40% to 45% may come from continued market-share gains. The economics increasingly favour scale players.

At the centre of Shadowfax’s strategy is network density. The company now operates across more than 15,600 pin codes through nearly 4,800 touchpoints, supported by roughly 2.6 Lakh quarterly delivery partners and more than 3,500 daily trucks.

The larger the network becomes, the lower the effective cost per shipment tends to fall. Warehouses, sorting centres and transportation routes begin generating operating leverage as order density rises. That leverage is now becoming visible in the company’s financial profile.

Partner expenses declined to 52.2% of revenue in Q4 FY26 from 56.4% a year earlier, while corporate overheads also improved. Adjusted EBITDA margin expanded roughly 400 basis points YoY.

Importantly, the company believes that the largest gains are still ahead. Executives suggested EBITDA margins could improve by roughly 100 to 120 basis points annually through FY28, before accelerating further as infrastructure utilisation rises.

“We are sacrificing near-term margins for long-term dominance,” was the underlying message running through the earnings discussion.

This philosophy explains the company’s unusually aggressive investment cycle. Shadowfax spent ₹185 Cr on capex in FY26 alone, nearly matching the ₹246 Cr it invested cumulatively from inception through FY25. Much of that spending went towards automation, sortation infrastructure, geographic expansion and technology systems.

One newly launched NCR sort centre offers capacity for 10 Lakh daily orders and throughput of 48,000 shipments per hour. Yet despite the spending surge, the company closed FY26 with ₹1,574 Cr in cash and virtually no debt.

How Quick Commerce Is Reshaping BusinessIf scale is the foundation of Shadowfax’s strategy, quick commerce may be its most important growth catalyst. The company now describes itself as India’s leading 3PL provider for quick-commerce platforms.

Unlike traditional ecommerce, where power is concentrated among a handful of giants, India’s quick commerce ecosystem is more distributed. Management said that the market now has six or seven meaningful players, reducing dependence on any single customer.

“There is no sort of leverage that any one partner has on 3PLs,” executives said during the call.

Quick commerce changes logistics economics fundamentally. Deliveries occur within tighter geographic radii, order frequencies are higher and customer demand becomes more predictable. This increases route density, improves delivery utilisation and shortens fulfilment cycles. For logistics companies, these dynamics can structurally improve margins.

Shadowfax’s hyperlocal business generated ₹232 Cr in revenue in Q4 FY26, up 32.1% YoY, while hyperlocal order volumes climbed nearly 30%.

But management appears focused on an even larger opportunity emerging beyond grocery delivery. Executives repeatedly highlighted what they described as the next phase of quick commerce — verticalised categories such as fashion, beauty, gourmet products, pet care and childcare. The players in these categories often lack the scale or operational sophistication to build dedicated fulfilment networks internally. Shadowfax wants to provide them with the infrastructure.

This strategy is driving one of the company’s most ambitious bets — dark stores. Shadowfax currently operates around 15 dark stores but plans to scale that number to 100 during FY27. Management disclosed that the pilot locations have already demonstrated attractive economics, with some generating gross margins above 20% and achieving profitability within three to four months.

“We spent a lot of time learning how they work,” executives said, explaining that the first phase was intentionally designed as a pilot before broader expansion.

The dark store initiative represents a major strategic evolution. Rather than simply transporting parcels, Shadowfax is increasingly embedding itself into inventory storage, fulfilment management, demand forecasting and localised warehousing. The deeper it becomes integrated into merchant operations, the harder it becomes to replace.

Shadowfax’s Competitive MoatOne of the least understood aspects of Shadowfax’s model may also be one of its biggest structural advantages. According to the management, essentially 100% of the company’s last-mile deliveries are “crowdsourced”.

Delivery partners operate on a per-order basis, rather than as part of a fixed employee fleet. Drivers may simultaneously handle ecommerce deliveries, quick-commerce shipments, food delivery and mobility-related work through the same ecosystem.

“Nothing like that exists in our country,” management said during the earnings call. The structure resembles a hybrid between a flexible gig-work marketplace and a national logistics network. It allows capacity to scale dynamically with demand rather than remaining fixed during slower periods.

That flexibility matters enormously in logistics, where utilisation often determines profitability. A driver network capable of moving fluidly across categories reduces idle capacity while improving route density and earnings potential for delivery partners themselves.

The same model also gives Shadowfax unusual flexibility as it expands into new verticals.

Its ‘Prime’ offering, which provides intra-city same-day delivery and inter-city next-day shipping, has already expanded to more than 120 cities. Initially designed for D2C brands, the service is now being extended aggressively toward India’s SME ecosystem through ‘Shadowfax 360’ — a self-service logistics platform launched during FY26.

The platform allows merchants to onboard automatically with no minimum order requirements and minimal human sales intervention. Management believes tens of thousands of smaller businesses entering India’s D2C economy can now be added to the network without proportionate increases in headcount.

The next wave of growth, the company said in its presentation, will come from SMEs entering D2C commerce at scale. Shadowfax is positioning itself as the logistics backbone supporting that migration.

The Next Phase: AI & Premium FreightEven as it scales core parcel delivery, Shadowfax is widening its ambitions into more specialised logistics categories.

Through its ‘Prime Large’ initiative, the company plans to launch large-appliance and heavy-shipment logistics in FY27. Executives said the segment offers stronger yields, higher barriers to entry and fewer national competitors.

“Pull-driven demand” already exists from customers, the company’s management said, because relatively few logistics providers currently possess the infrastructure needed to move heavy goods efficiently across India at scale.

At the same time, the acquisition of CriticaLog adds a premium freight and high-value logistics layer to the broader ecosystem. The business specialises in time-sensitive shipments, luxury goods and critical logistics services, areas typically associated with higher margins and stronger customer stickiness.

The management described the acquisition as a strategic portfolio expansion rather than a diversification experiment. “Portfolio gap closed without new build-out,” the company said in its presentation.

Underlying many of these initiatives is another recurring theme — artificial intelligence (AI).

Executives repeatedly referenced AI-driven routing, node prioritisation, image recognition, demand forecasting and quality-control systems. In logistics, even small optimisation improvements can compound dramatically at scale. Faster routing decisions, better warehouse placement and improved shipment visibility can materially lower costs across millions of daily deliveries.

Still, risks remain substantial. India’s logistics sector remains intensely competitive, particularly as quick commerce platforms continue experimenting with internal fulfilment capabilities. Operational complexity is also rising rapidly as Shadowfax simultaneously scales automation, dark stores, SME onboarding, heavy logistics and premium freight.

Loss-shipment and quality-check costs remain elevated at more than 6% of revenue, though the company’s management said technology investments should gradually reduce those figures over time.

Yet, Shadowfax’s current trajectory suggests that the company may already have crossed an important threshold.

For years, Indian logistics startups were forced to choose between rapid growth and sustainable profitability. Shadowfax appears to have achieved both simultaneously in FY26 — 69.1% revenue growth, 66.4% order growth, expanding margins, a net profit of ₹112 Cr, and accelerating market share gains.

This is why FY26 increasingly looks less like a strong operating year and more like an inflection point for Shadowfax. The company that once competed simply to deliver packages is now trying to build the infrastructure layer beneath India’s digital economy itself.

The post Shadowfax’s Inflection Point And The Next Frontier appeared first on Inc42 Media.

-

Invest Just ₹12,000 Monthly and Build a ₹2 Crore Retirement Fund; Here’s the Full Calculation

-

Save Tax and Build Wealth Together: 4 Smart Investment Options You Should Know

-

Gold Price Jumps by ₹6,500 in a Week, Silver Surges ₹5,000; Check Latest Rates in Major Cities

-

8th Pay Commission: Big Demand on Basic Pay and DA Could Trigger Massive Salary Hike for Central Employees

-

Babar Azam Matches Steve Smith's Massive World Test Championship Record