India is in the middle of a boom in financial inclusion with an increasing number of households getting access to credit. No wonder, household debt has scaled its peak of 42% of the GDP.

The ease of credit from a rising number of digital lending platforms and fintechs pushed the share of final private consumption expenditure (PFCE) in GDP to 61.5% in FY26. But the surge in the new-to-credit borrowers has exposed gaps in the traditional lending practices, especially in terms of collections.

Without strong collection practices, lenders run the risk of accumulating NPAs. They rely on third-party collection agencies, which largely operate through inefficient manual processes. The middlemen they deploy are infamous for unethical tactics like harassing and intimidating borrowers.

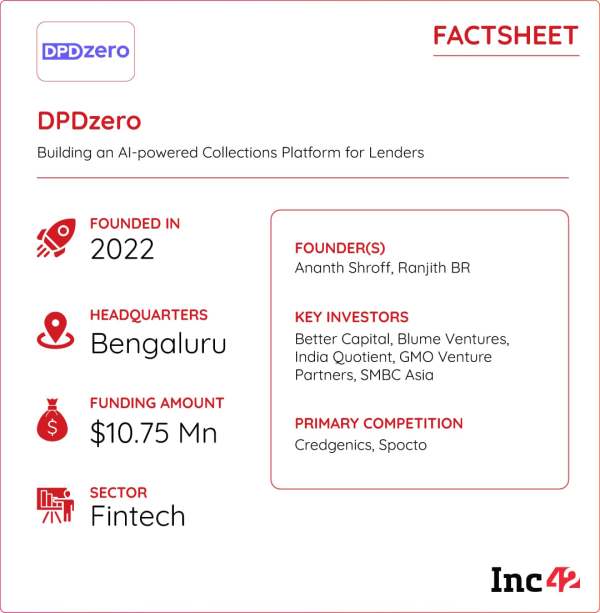

Seeing the challenges in this highly fragmented space, Ananth Shroff and Ranjith BR spotted an opportunity to build the rails for a tech-based collections platform. In 2022, the duo founded DPDzero to offer lenders a plug-and-play solution that could help them handle recoveries in a transparent, efficient and ethical manner. The name DPDzeo was adapted from the mission of ‘zero days past due’ that helps lenders to collect every payment on time.

The concept has attracted investor interest with financiers like Better Capital, Blume Ventures and India Quotient pumping nearly $11 Mn into the company in three rounds so far. In its most recent Series A round, Japanese fintech investor GMO Venture Partners and Japanese financial heavyweight SMBC Asia too joined the captable.

After tying up with several NBFCs and fintechs, DPDzero looks to build partnerships with banks as well. The startup has more than 30 lenders like RBL Bank, IndusInd Bank, L&T Finance, Tata Capital, Poonawalla Fincorp, Kreditbee and Moneyview on its client list. The Bengaluru-based company wants to support the growth of credit penetration with an education-focussed and a tech-driven approach to collections.

The seeds of DPDzero germinated during the days when Shroff and Ranjith worked as part of the founding team of Setu. They built tech infrastructure to connect fintechs with banks and NBFCs. When Setu was acquired by Pine Labs in 2022, they decided to roll out a venture that would continue building their previous work of enabling access to formal credit for the underserved populace.

They identified the four pillars of lending – capital, customer acquisition, underwriting, and collections – to build their business. While most financial institutions had ready access to capital and the boom in smartphone penetration was helping in customer acquisition, lenders generally preferred to keep their underwriting processes proprietary, rather than relying on external startups. Hence, they positioned their business to solve gaps in collections.

“Collections is a completely fragmented and unorganised space where there is no technology and no transparency. If we are able to build a highly scalable pan-India collections infrastructure, that can enable a lender to plug in while absorbing all the operational complexity, that would lead to hyperscaling for lending institutions in the country,” CEO Shroff told Inc42.

But, tech alone wasn’t enough to solve such a deepening problem, they knew. The company also directly employs its own collection agents to call up borrowers, and field agents to pay them a visit in person when necessary. DPDzero calls these employees ‘advisors’, instead of collection agents, to reinforce the idea that their role is to inform and educate the borrower on how to clear their dues rather than threatening them. It also invests in training them according to its code of ethics, and uses its AI platform to guide them in their interactions with borrowers.

The Reserve Bank of India, too, thrashed out guidelines, making it mandatory to deploy collection agents only after they’re trained. The regulator’s action was triggered by an increasing number of complaints of harassment from borrowers.

“In this business, humans play the most important role. Our human advisors create assets that we use to train our AI voice agents, which is how it becomes better every day,” Shroff said. “Around 99.5% of borrowers are not bad. The 0.5% are tricky. They are unaware, but not bad. But the industry treats 100% as 0.5%.”

Using Tech to Streamline EfficiencyInc42 dug into the DPDzero tech stack to comprehend how it replaces human intervention to avoid any undesired situation for the borrower as well as assure full return to the lender.

“Today, collection agencies are small businesses with 30-100 agents. They mostly work out of an Excel sheet or a dialler (calling software), and they call up borrowers, track them manually, and follow up with them. Around 60% of the activities are driven by individuals and 40% by the software,” explained Shroff.

DPDzero uses technology at every step along the way. Once a lending institution partners with them, they merely need to make the decision to route a particular loan portfolio to the startup. Then, the data package is pushed to DPDzero’s AI-powered platform through an API and processed. The AI then analyses the profiles of various borrowers and their dues, groups them into segments, and recommends the best way to move forward for each group. For example, a borrower whose EMIs are due on the 1st of the month but usually pays on the 5th, perhaps because of a gap between the due date and the date of getting the salary, is considered low-risk, while a borrower whose payments are irregular is considered high-risk.

Based on this analysis, the AI platform decides the best channel to reach a borrower. An AI voice agent is sufficient to call up a low-risk borrower, while a human advisor would call up a relatively high-risk borrower and speak to them in tandem with live recommendations given by AI that would optimise the probability of recovery. For cases where neither might be able to reach the borrower, DPDzero has recently started employing field advisors who come to the borrower’s doorstep to speak to them directly.

“We have a lot of new-to-credit borrowers because our exposure to unsecured loans is high. Borrowers from a Tier-II or Tier-III town who have upgraded to an NBFC for the first time lack an understanding of credit and the responsibility they own when they take credit,” Shroff pointed out.

DPDzero’s system, accordingly, profiles borrowers on the reason why they have missed paying their dues in a way that informs the advisors’ approach. When it comes to those deemed intentionally delinquent, the advisor focuses on explaining how their credit score works and the consequences of their credit score dipping as a result of loan defaults.

There are also circumstantial defaulters who have missed repayments due to losing their job or unforeseen financial issues like medical expenses. In these cases, the advisor needs to focus on explaining what options the borrower has. “What we do is tell them that they can withdraw from their PF, break their FDs, sell off some gold to pay off the obligations. We give them options to be debt-free first so that they can peacefully focus on their life and search for their job,” Shroff said.

“DPDzero enables every lending institution to run collections on autopilot, unifying all the channels from AI voice agents to human calling agents to field agents in a single infrastructure, optimising which channel to use for what borrower to get the best results at the lowest cost.”

Framing A Unique Business ModelUsing technology to fix collection issues is not unique. Well-funded rivals like Spocto and Credgenics also operate in the same space. But DPDzero has a unique outcome-based pricing model that edges out its rivals.

“We understood very early that if you do not control the outcomes, you are not going to become a meaningful partner to large financial institutions. So, from day one, we have only charged on success. We are the first to have an outcome-based commercial model where we only get paid once we get the money back to you,” Shroff claimed.

Once the partner commits a certain portfolio, DPDzero charges them a certain percentage of the pending dues as its fee. It uses a tech-based pricing model that determines how much effort the recovery would require, based on the type of loans, delinquency level, average ticket size, pin code, past behaviour of the customers, and other parameters. Then, the partner only needs to pay DPDzero after it delivers the dues.

The model works because DPDzero focuses on serving them from two perspectives – minimising NPAs and bringing down the costs. The company claims it has been able to reduce NPAs by over 22% on a blended basis across lenders. When working with lenders who are more concerned with the cost of recovering later-stage delinquencies, it has reduced their cost by up to 30%.

The model paid off as DPDzero tripled its revenue in the last one year, though Shroff declined to share specific figures. “On a monthly basis, we manage around INR 2,000 Cr portfolio across 22 lakh borrowers,” he said. For the short term, the company plans to grow the monthly portfolio to INR 5,000 Cr while also hiring more leaders across functions. “We have been scaling rapidly and have now hit the next level of growth so we are building leadership.”

DPDzero is also investing in technology so that its AI platform can not only give better nudges to the human advisors, but also to improve its AI voice agents to close more cases without human intervention. The company is also building up its on-ground presence by hiring more field advisors across multiple states and bringing in the right expertise to train them so that they recover dues while continuing to act in accordance with its code of conduct.

Mapping The Way AheadThe march of the world’s fastest-growing major economy at 6.8% to 7.2% in FY27 faces a challenge of a growth in loan defaults, especially small-ticket loans and in rural areas, with overdues by over 90 days going up to 3.6% in 2025. Defaults are higher in Tier III towns, among young borrowers, and people with little credit history.

Unpaid credit card dues too are also growing quickly, pushing up the gross bad debt for banks and financial institutions. Aggressive lending by non-bank financiers and fintech startups, often in violation of stricter RBI rules on weighted average rates, has escalated the concern.

The gross bad loan ratios of private banks rose 1-14 basis points in the October-December period from the preceding quarter to range between 1.42% and 4.7% of total loans. One basis point is one-hundredth of a percentage point. The Reserve Bank predicts a 3% rise in NPA by March 2026 from a 12-year low of 2.6% in September 2024.

Given such a backdrop of sour loans, DPDzero sees itself at a sweet spot to push its tech solutions as a smarter solution for challenges plaguing the collections space.

The post Can DPDzero’s AI Bet End The Fear Around Debt Recovery, Collections? appeared first on Inc42 Media.

-

The increased fat on the stomach will decrease within a month! Include fiber rich foods in your daily diet

-

Accident – Luxury Car Crash in Kanpur Leaves Six Injured

-

Employment – Shivpuri Youth Builds Respect Through Small Juice Stall

-

Unemployment – J&K Government Earns Rs 48 Crore from Job Applications

-

PowerSector – Jammu and Kashmir Plans Major Hydropower Expansion by 2031